Blog > Feeling Trapped by Your 3% Mortgage Rate? You Have To You Don't Have To Be

Feeling Trapped by Your 3% Mortgage Rate? You Have To You Don't Have To Be

by

Feeling Trapped by Your 3% Mortgage Rate? You Have To You Don't Have To Be

If you bought or refinanced your home during 2020 or 2021, there’s a good chance you’re sitting on a mortgage somewhere around 3%.

That is one of the best financial deals you may ever receive.

It has also become one of the biggest reasons many homeowners in Carlsbad, Encinitas, Solana Beach, Oceanside, and San Marcos are not moving, even when they want to.

The headlines call it the “rate lock-in effect.” That is accurate, but it barely scratches the surface.

The real question is not whether your 3% mortgage is valuable.

It is.

The better question is this:

Is keeping that mortgage producing the best overall financial outcome for your life, your family, and your long-term wealth?

Those are two very different questions.

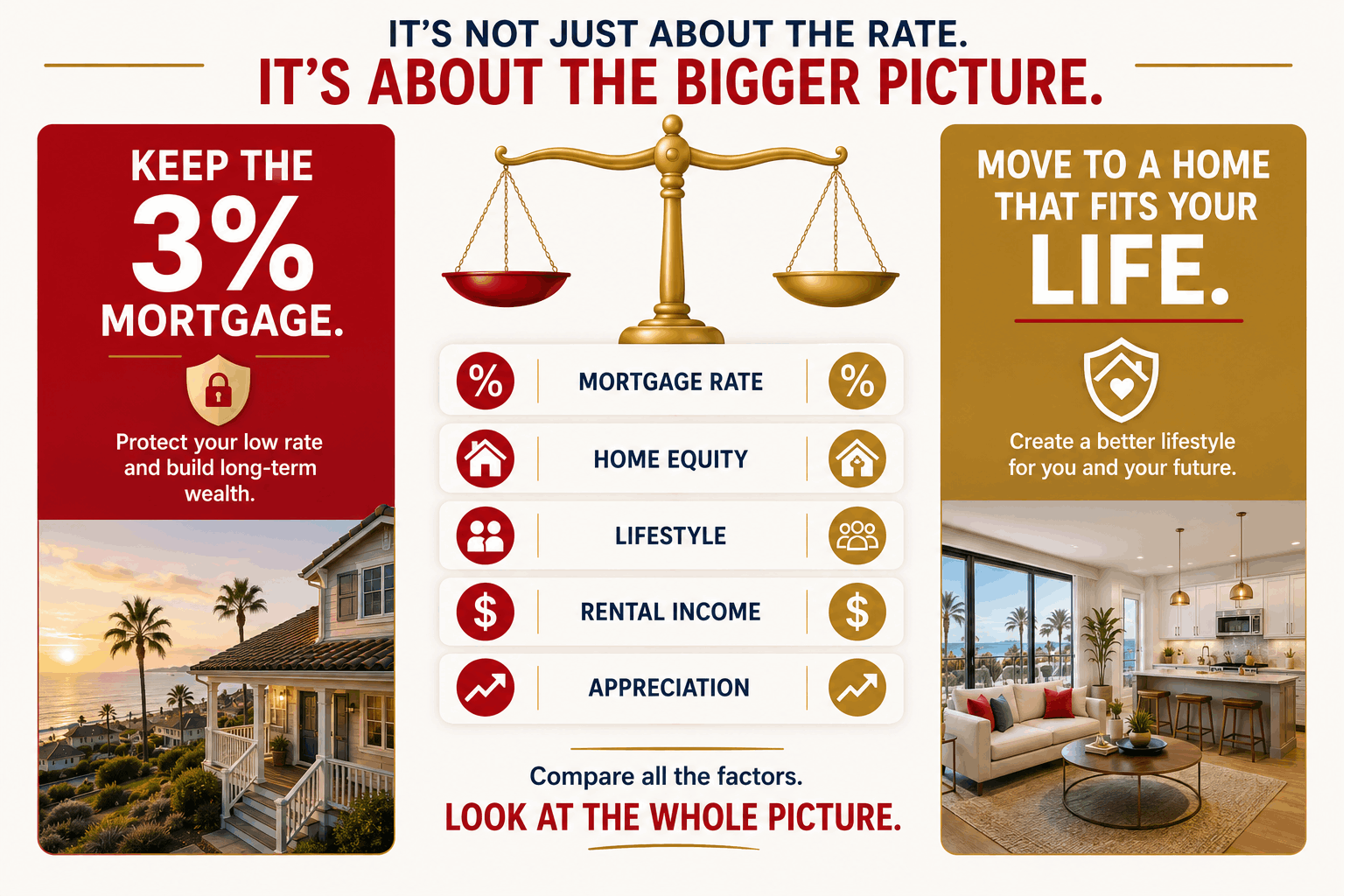

The Biggest Mistake: Comparing Interest Rates Instead of Net Wealth

Most homeowners mentally compare one number:

3% versus 6.5%, or whatever today’s rates happen to be.

That comparison feels painful. But it ignores almost everything else that matters.

Before deciding you are “stuck,” ask yourself:

- How much equity has your home gained?

- Would a different home better fit your family’s needs?

- Could your current property become an income-producing asset?

- What is the financial cost of delaying a move for another five years?

- How much are you spending maintaining a home that no longer fits your lifestyle?

- Are you protecting a low rate while ignoring larger financial opportunities?

A mortgage rate is one variable.

Your overall balance sheet is the bigger picture.

Coastal North County Is Different

This conversation looks very different in coastal North County San Diego than it does in many other parts of the country.

Many homeowners purchased before prices accelerated dramatically. That means it is common to see homeowners with $700,000 to over $1 million in equity, along with relatively low monthly payments.

At the same time, coastal communities continue to attract renters because buying remains expensive.

That combination creates options many homeowners do not realize they have.

Option One: Keep the 3% Loan... But Keep the House Too

One overlooked strategy is converting your current home into a rental rather than selling it.

Suppose your situation looks something like this:

- Current home value: $1.9 million

- Mortgage balance: $650,000 at 3%

- Monthly principal and interest: about $2,740

- Taxes and insurance: roughly $1,400 per month

- Total housing payment: approximately $4,440 per month

If that property rents for around $5,800 to $8,000 or more per month, depending on size, location, condition, and neighborhood, the numbers may work surprisingly well.

Instead of giving up a 3% loan, you preserve it while letting a tenant help pay it down.

Meanwhile, you purchase your next home separately.

This approach is not right for everyone. Being a landlord comes with responsibilities. Vacancies happen. Repairs happen. Cash reserves matter.

But in North County’s rental market, it is a strategy worth analyzing before automatically listing your home.

Option Two: Buy First, Sell Later

One reason homeowners hesitate to move is uncertainty.

They wonder:

“What if I sell and cannot find the next house?”

That is a legitimate concern.

Several financing tools may reduce that pressure:

- A HELOC may provide access to equity before selling.

- A bridge loan may allow you to purchase the replacement home before your current one closes.

- Strong equity may give you more flexibility when structuring the next purchase.

- Buying first can reduce the pressure of trying to coordinate two transactions at the same time.

For homeowners with substantial equity, buying first may lead to better negotiating decisions because they are not trying to sell, buy, move, and make rushed choices all in the same weekend.

These tools are not for every borrower, and qualification requirements vary.

But they are frequently overlooked because many homeowners assume selling first is the only option.

Option Three: Reduce the Effective Rate Instead of Chasing Yesterday’s Rate

Many buyers become fixated on today’s advertised mortgage rate.

But that is not always the rate you actually live with.

There may be ways to reduce the effective cost of financing, including:

- Seller-paid temporary rate buydowns

- Permanent discount points

- Larger down payments from accumulated equity

- Smaller mortgage balances after selling a high-equity property

- Strategic loan structuring based on your long-term plans

A 6.5% loan on a much smaller balance is very different from a 6.5% loan on a first home with only 5% down.

The effective cost of financing depends on the entire structure of the purchase, not just the headline interest rate.

Option Four: Do Not Overlook Assumable Loans

Assumable loans are not discussed nearly enough.

Some mortgages, particularly many FHA and VA loans, may be assumable.

That means a qualified buyer may be able to take over the seller’s existing mortgage rather than obtaining an entirely new loan.

That can matter if the existing loan has a rate far below current market rates.

Assumable financing has qualification requirements, and not every loan qualifies. In higher-priced coastal North County markets, the number of assumable loan opportunities may also be limited.

But if your loan qualifies, it could become a meaningful advantage when marketing your home.

A buyer may be attracted to financing that is well below current market rates.

That is one more reason every homeowner should understand exactly what type of loan they have before deciding their next move.

The Math Most Homeowners Never Actually Run

Let’s use a simplified example.

A Carlsbad homeowner purchased for $900,000.

Today the property is worth approximately $1.7 million.

That is roughly $800,000 in appreciation before selling costs.

Many homeowners immediately think:

“I would never give up my 3% mortgage.”

But here is another way to view the same situation:

Would you decline access to hundreds of thousands of dollars in equity simply to preserve a low interest rate?

Sometimes the answer is yes.

Often, it is not that simple.

Now add another variable.

Suppose the family has outgrown the home:

- Kids are sharing bedrooms.

- One spouse now works remotely without dedicated office space.

- The commute has become exhausting.

- The home requires more maintenance than the family wants to handle.

- The layout no longer fits the way they live.

Remaining in the property is not free.

There are opportunity costs that never appear on a mortgage statement.

Lifestyle has value too.

Sometimes Staying Put Is Exactly the Right Decision

Not every homeowner should move.

Sometimes the current home remains the best financial choice.

Sometimes converting it to a rental creates long-term wealth.

Sometimes selling and simplifying life produces a better outcome.

Sometimes downsizing unlocks equity while lowering ongoing expenses.

The point is simple:

Your mortgage rate should inform the decision.

It should not make the decision for you.

Every Situation Is Different

The homeowners I meet throughout Carlsbad, Encinitas, Oceanside, Solana Beach, and San Marcos all have different priorities.

Some want more space.

Some want less maintenance.

Some want to help aging parents.

Others want to reduce expenses before retirement.

The right answer usually comes from comparing multiple scenarios, not reacting to one interest rate.

A careful side-by-side analysis can estimate what happens if you:

- Stay where you are

- Sell and buy another home

- Keep your current property as a rental

- Use your equity strategically before selling

- Downsize and reduce monthly expenses

- Buy first and sell later

- Explore whether your current loan has any assumable value

Seeing those numbers on paper often changes the conversation.

Are You Really Stuck, or Just Missing the Full Picture?

If you have been wondering whether you are truly “stuck” because of your 3% mortgage, I would be happy to help you evaluate the options objectively.

I am Rob Denny, a Carlsbad-based real estate agent with HomeSmart Realty West, and I work with homeowners throughout coastal North County San Diego.

Rather than offering generic advice, I can help you compare the financial impact of each path based on your home’s equity, your financing options, and your long-term goals.

That way, you can make a decision backed by numbers instead of assumptions.

Call or text Rob Denny at 858-504-0449 to talk through your options.